Issuing shares to an employee

2nd September 2021

Posted in Articles by Michael Hodgson

The issue

Companies will often seek to reward and incentivise employees with shares rather than cash bonuses. Where shares are issued to an employee for free (or below the current market value) there will generally be significant tax consequences. The value of the shares will be treated as employment income, subject to income tax and potentially national insurance.

Share options are often appropriate and where issued under an approved scheme, can defer the tax cost to a point where the company is sold. At that point, the option holder receives cash proceeds, which cover the cost of acquiring the shares. However, there are occasions where the company will want to issue actual shares at the outset to the employee. This may be because:

- The shareholders have no intention of selling the company for the foreseeable future;

- The company would like to pay dividends to the individual;

- Or simply, the shareholders want the employee to feel ‘part of the club’ and have physical shares.

Unless the employee pays full market value (‘MV’) for the shares, there is always going to be a tax cost. The question therefore arises: how can the company minimise the tax cost arising on issuing shares to an employee for free?

Issuing the shares through an EMI scheme

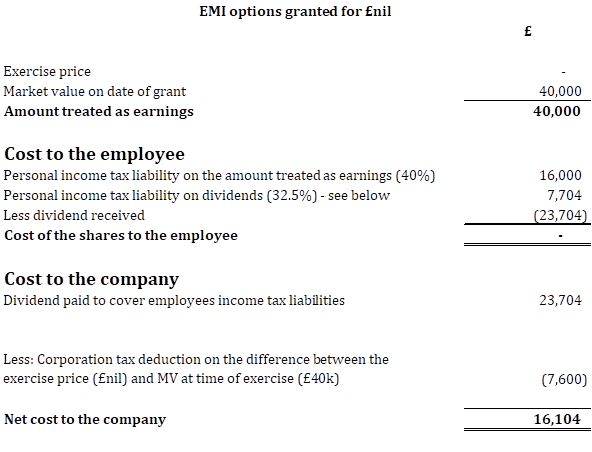

Issuing EMI options to the individual with a £nil exercise price is often overlooked, however, it can often be the most tax efficient route if providing shares way before any intended sale. Care must be taken to demonstrate that the intention was to retain and motivate the employee and not solely to provide a tax benefit.

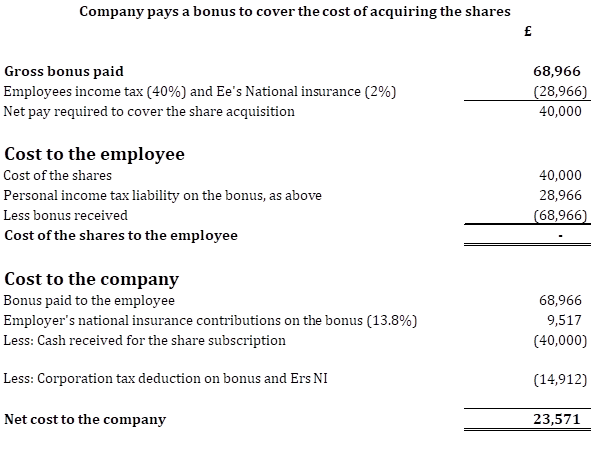

The below worked example, shows how issuing ‘free’ shares worth £40,000, through an EMI scheme can save the company nearly £7,500, when compared to the company paying a bonus to cover the cost of acquiring the shares.

There are of course other ways for the company to cover the cost of acquiring the shares, such as paying a grossed-up dividend to the employee once in receipt of the shares. However, this still presents a short-term problem of how the initial acquisition of the shares is funded and generally still results in a higher total cost for the Company.

The main tax benefits arising from using an EMI scheme are:

- The company obtains a corporation tax deduction on the difference between the £nil exercise price and the market value at the time of exercise.

- The company and share valuation can be agreed in advance with HMRC. This removes the possibility that HMRC will later argue a different value.

Forbes Dawson view

Issuing share options at below market value is rarely considered, this is probably because, the majority of options are only exercisable immediately before a sale and in this case there will normally be little benefit in doing so. This is because the shares are likely to be readily convertible assets upon which national insurance would be payable. However, in certain circumstances it may well be the most tax efficient option.

The above scenario also highlights the importance of obtaining appropriate tax advice when considering how best to structure a company’s affairs, as the most tax efficient options are not always immediately clear.